What Is a 1031 Exchange?

A $450K gain on a coastal property triggers $173K in combined federal and state tax—fully deferrable with a 1031 exchange.

View chart data

| Category | Tax liability ($) |

|---|---|

| Capital Gain | $450k |

| Federal Tax (23.8%) | -$107k |

| State Tax (13.3%) | -$60k |

| Depreciation Recapture (25%) | -$20k |

| Total Tax Owed | -$187k |

| Tax Deferred | $187k |

A 1031 exchange — named after IRC §1031 — lets you sell an investment property and buy another without paying capital gains tax on the sale. The tax isn't forgiven; it's deferred. When you eventually sell the replacement property (outside of another 1031), you'll owe tax on the original gain plus any new appreciation. But in the meantime, you keep 100% of your equity working.

Interactive Tool

1031 Exchange Tax Deferral Calculator

Estimate the capital gains tax you can defer by rolling proceeds into a replacement property.

Depreciation recapture is taxed at 25% federal.

Here's the math. Say you bought a Costa Mesa duplex in 2015 for $650,000. You sell it today for $1.1 million. Your gain is $450,000. Federal capital gains tax at 20% plus 3.8% net investment income tax plus California state tax at 13.3% means you're looking at roughly $167,000 in combined tax. If you do a 1031 exchange and roll the full $1.1 million into a replacement property, you defer that $167,000 and buy a bigger asset with the entire proceeds.

Most small landlords I talk to assume 1031 exchanges are only for big commercial players or that the paperwork is prohibitively complex. Neither is true. The rules are strict, but they're not complicated. You just have to follow them exactly.

The Like-Kind Requirement Is Broader Than You Think

Under the 2017 Tax Cuts and Jobs Act, 1031 exchanges now apply only to real property — not boats, art, or equipment. But within real property, the like-kind standard is extremely broad. Any investment real estate can exchange for any other investment real estate, regardless of property type, location, or condition.

That means:

- A Newport Beach single-family rental can trade for a Riverside fourplex.

- A beachfront condo in Laguna can trade for a suburban office building in Irvine.

- A coastal vacation rental can trade for a long-term multifamily property 40 miles inland.

- Raw land held for investment can trade for an income-producing duplex.

The only hard rule: both properties must be held for investment or business use. You can't exchange your primary residence (unless you convert it to a rental first and hold it for a reasonable period — typically two years). You can't exchange a fix-and-flip you held for 90 days. The IRS looks for investment intent, and the safe harbor is a minimum holding period of one to two years before and after the exchange.

Look, I've had owners ask if they can trade a coastal SFR for a Texas multifamily. Yes. Different state, different asset class — still like-kind. The only thing that matters is that both are investment real estate.

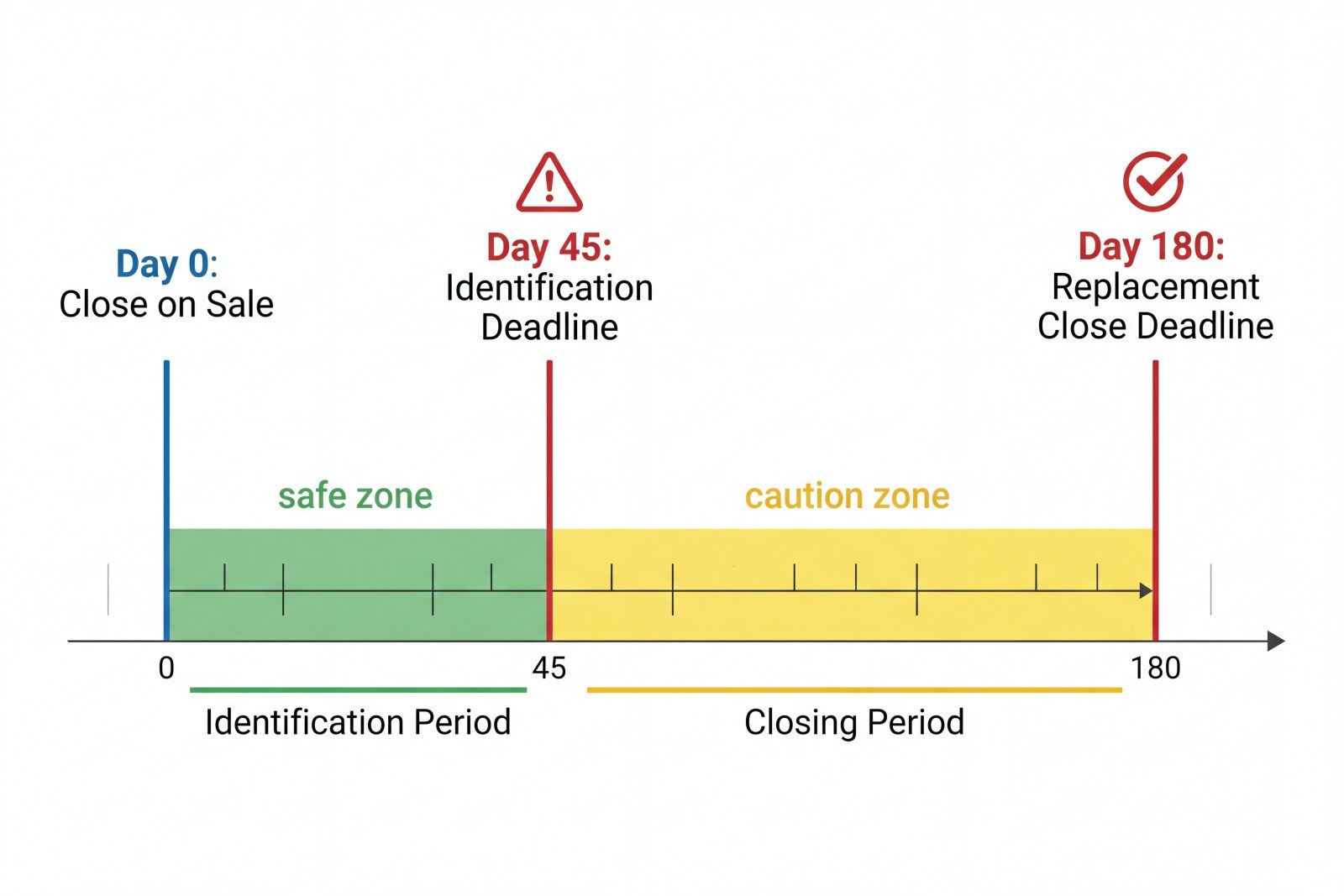

The 45-Day and 180-Day Windows

The 1031 timeline is the part that kills deals. Miss a deadline by one day and the entire exchange fails — you owe tax on the full gain.

Here's how it works. Day zero is the day you close on the sale of your relinquished property (the one you're selling). From that date:

- 45 calendar days to identify replacement properties in writing to your qualified intermediary.

- 180 calendar days to close on at least one of those identified properties.

Both deadlines run concurrently, so the 180-day clock starts on day zero, not after the 45-day ID period. And both are calendar days — weekends and holidays count. If day 45 falls on a Saturday, your identification is due Saturday. No extensions.

The identification rules give you three options:

- Three-Property Rule: Identify up to three properties of any value. You must close on at least one.

- 200% Rule: Identify any number of properties as long as their combined fair market value doesn't exceed 200% of the relinquished property's sale price.

- 95% Rule: Identify any number of properties of any total value, but you must close on properties representing at least 95% of the total identified value.

Most small landlords use the three-property rule. You identify three potential replacements, then close on whichever deal comes together first. The identification must be in writing, signed, and delivered to the intermediary by midnight on day 45. Email works. Fax works. A verbal list does not work.

Honestly, the 45-day window is tight. You're shopping for a replacement property while also managing the close of your sale. Start looking before you list the relinquished property. Have a shortlist ready. The clock starts the day escrow closes, and 45 days disappears fast.

You Must Use a Qualified Intermediary

You cannot touch the sale proceeds. If the buyer wires funds to your bank account, even for one day, the exchange is blown and you owe tax on the full gain. The money must go directly to a qualified intermediary — a third-party company that holds the funds in escrow and then uses them to buy the replacement property on your behalf.

The intermediary can't be someone you have a close relationship with. The IRS disqualifies:

- Your CPA or tax preparer (within the past two years).

- Your attorney (within the past two years).

- Your real estate agent or broker.

- Your employee.

- A family member.

- Anyone who has acted as your agent in the past two years.

You hire a professional intermediary — usually a company that does nothing but 1031 exchanges. They charge a flat fee, typically $800 to $1,500 for a straightforward exchange. They draft the exchange agreement, hold the funds, prepare the assignment documents, and coordinate with both escrow companies.

The intermediary must be in place before you close on the sale. You can't sell the property, realize you want to do a 1031, and then hire an intermediary retroactively. The exchange structure has to exist at the time of sale.

Boot and Debt-Replacement Gotchas

To defer 100% of the gain, you must follow two reinvestment rules:

- Equal or greater value: The replacement property must have a purchase price equal to or greater than the net sale price of the relinquished property.

- Equal or greater debt: The debt on the replacement property must be equal to or greater than the debt paid off on the relinquished property — or you must add cash to make up the difference.

If you violate either rule, you receive 'boot' — taxable proceeds. Boot is taxed as capital gain in the year of the exchange.

Here's an example. You sell a property for $900,000 with a $400,000 mortgage. Net proceeds are $500,000 (ignoring closing costs for simplicity). You buy a replacement property for $850,000 with a $350,000 mortgage and $500,000 down. You've reinvested all the cash, but you've reduced your debt by $50,000. That $50,000 is mortgage boot, and it's taxable.

To avoid boot, the replacement property must cost at least $900,000 and carry at least $400,000 in debt. If you want to pay all cash on the replacement, you'd need to add $400,000 of new cash to offset the debt relief.

Cash boot is simpler: if you take any cash out at closing — even $5,000 for a new roof or to cover a gap — that cash is taxable. The intermediary must use 100% of the proceeds to buy the replacement. If there's money left over after the purchase, it gets distributed to you and taxed.

Most small landlords I work with trip on the debt rule. They assume rolling all the cash forward is enough. It's not. The debt has to roll forward too, or you pay tax on the relief.

The Related-Party Rule

You can't do a 1031 exchange with a related party unless both you and the related party hold the properties for at least two years after the exchange. Related parties include:

- Family members (spouse, siblings, parents, children, grandparents, grandchildren).

- Entities you control (your LLC, your S-corp, your partnership if you own more than 50%).

- Trusts where you're a beneficiary.

The IRS added this rule to prevent tax-free basis step-ups between family members. If you sell to your brother and he sells to a third party six months later, the IRS treats the whole chain as a taxable sale.

If you do exchange with a related party, both properties must be held for two years. If either party disposes of their property within that window, both exchanges are retroactively disqualified and you owe tax plus interest.

There's an exception for involuntary conversions (death, condemnation, foreclosure), but for voluntary sales the two-year hold is absolute.

Reverse Exchanges (When You Buy First)

Sometimes you find the perfect replacement property before you've sold the relinquished property. A reverse exchange lets you buy first and sell later, but the mechanics are more complex and the costs are higher.

In a reverse exchange, the intermediary takes title to the replacement property (using your funds) and holds it in a parking arrangement while you sell the relinquished property. Once that sale closes, the intermediary transfers the replacement property to you and the exchange is complete.

The same 45-day and 180-day rules apply, but they run in reverse: you have 45 days from the date the intermediary acquires the replacement to identify the relinquished property, and 180 days to close the sale.

Reverse exchanges cost more — typically $3,000 to $5,000 in intermediary fees, plus the cost of holding title (property insurance, property tax, any debt service if the intermediary finances the purchase). They're also harder to finance, because the intermediary is the borrower of record during the parking period.

Most small landlords don't need a reverse exchange. If you can time the sale and purchase to close within a few weeks of each other, a standard forward exchange works fine. But if you're in a hot market and you need to lock up the replacement before you list the relinquished property, a reverse exchange is the tool.

Pre-Exchange Checklist

Before you list your property for sale, run through this checklist:

- Hire a qualified intermediary. Do this before you open escrow on the sale. Get the exchange agreement signed.

- Confirm investment intent. Make sure you've held the relinquished property for at least one to two years and you plan to hold the replacement for at least one to two years. If the IRS thinks you're flipping, the exchange fails.

- Start shopping for replacements. Don't wait until after the sale closes. You need a shortlist ready so you can identify within 45 days.

- Check your debt structure. If you're paying off a mortgage on the relinquished property, make sure the replacement property will carry equal or greater debt — or plan to add cash.

- Avoid related-party transactions. If you're buying from or selling to family or an entity you control, consult a tax advisor. The two-year hold requirement is strict.

- Coordinate with your CPA. Your CPA can't be your intermediary, but they should review the exchange structure and prepare Form 8824 for your tax return.

- Plan for no cash out. If you need cash from the sale for any reason, take it before the exchange or plan to pay tax on it as boot.

The 1031 exchange is the single most powerful tax-deferral tool available to rental property owners. But it's unforgiving — miss a deadline, take cash out, or violate the debt rule, and you lose the deferral. The key is planning early and following the rules exactly.

Common Questions I Get

Can I do a 1031 exchange on a property I've been renting on Airbnb? Yes, as long as you've held it as an investment property and you're exchanging into another investment property. The IRS has ruled that short-term vacation rentals qualify for 1031 treatment if they're held for investment (not personal use). If you've been blocking out weeks for your own vacations, that's a problem — personal use disqualifies the property. But if it's been rented to third parties full-time, you're fine.

What happens if I identify three properties but only one deal closes? That's fine. The three-property rule lets you identify up to three; you only need to close on one. The other two can fall through.

Can I use 1031 exchange proceeds as a down payment and finance the rest? Yes. The intermediary uses your proceeds as the down payment, and you get a mortgage for the balance. Just make sure the total purchase price and total debt meet the reinvestment rules.

Do I have to buy in California? No. You can exchange a California property for a property in any state. The like-kind rule is federal, and it applies nationwide.

What if I can't find a replacement property in 180 days? The exchange fails and you owe tax on the gain. There are no extensions. In a tight market, this is a real risk — which is why you should start shopping before you close the sale.

Frequently Asked Questions

How long do I have to identify a replacement property in a 1031 exchange?

Can I do a 1031 exchange if I sell a single-family rental and buy a multifamily property?

What is boot in a 1031 exchange?

Do I need to use a qualified intermediary for a 1031 exchange?

Can I exchange a California rental property for a property in another state?