What Is a Reverse 1031 Exchange?

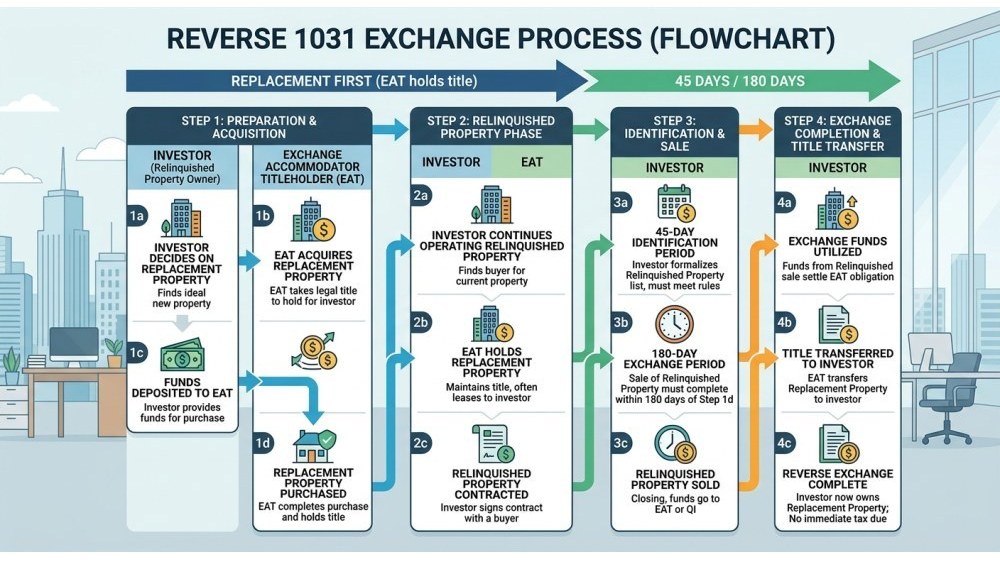

In a reverse 1031 exchange, you take title to the replacement property before you sell the relinquished asset, deferring capital-gains tax under IRC Section 1031 despite the inverted sequence. Revenue Procedure 2000-37 established the safe-harbor framework in 2000, permitting a 180-day combined timeline to acquire the replacement property and dispose of the old one.

Section 1031 bars simultaneous ownership of both properties, so you rely on an Exchange Accommodation Titleholder (EAT), a special-purpose entity that holds bare legal title to one asset (typically the replacement) while you retain all economic risk, management authority, and operating control. The EAT exists solely to satisfy the non-overlap requirement; you fund the acquisition, collect the rent, pay the expenses, and absorb price movements during the parking period.

Reverse structures represent a measurable fraction of total 1031 activity. In supply-starved coastal markets where beachfront inventory moves quickly, reverse exchanges account for a disproportionate share of high-value single-family rental transactions, driven by competitive pressure and the need to lock in scarce oceanfront or hillside-view properties before they trade.

Mechanics: Parking Arrangements and Title Holding

Revenue Procedure 2000-37 defines two configurations. Under a reverse exchange parking arrangement, the EAT takes title to the replacement property while you continue to own the relinquished asset and prepare it for sale. Under a reverse exchange improvement parking arrangement, the EAT holds the replacement property and funds construction or capital improvements before the exchange closes, a structure useful when acquiring a teardown lot or a coastal asset requiring immediate renovation to reach stabilized occupancy.

The parking period runs 180 calendar days from the date the EAT records title. You must submit written identification of the relinquished property (if the EAT is parking the replacement) or the replacement property (if the EAT is parking the relinquished) within the first 45 days. The qualified intermediary receives this identification, which becomes binding once filed.

Title resides with the EAT, but every economic incident of ownership flows to you. You wire the purchase funds, remit property tax, maintain insurance, pay HOA assessments, and service any debt. Rental income accrues to you; unrealized losses land on your balance sheet. The EAT performs no substantive function beyond holding legal title to satisfy Section 1031's prohibition on overlapping ownership.

Qualified Intermediary and EAT Relationship

The EAT is usually a single-member LLC formed by your qualified intermediary for this transaction alone. The QI acts as manager, executes documents in the EAT's name, and enforces safe-harbor compliance. You cannot serve as the EAT, nor can any disqualified person: your agent, attorney, accountant, employee, or family member who has acted in one of those capacities within the prior two years.

The QI charges incremental fees for reverse exchange services, including a setup fee to form the EAT, monthly holding fees throughout the parking period, and legal documentation costs. These fees layer on top of standard QI exchange fees and reflect the intermediary's assumption of title liability, elevated compliance risk, and the need to maintain separate books and records for a high-value asset over a six-month window.

Capital Requirements and Financing Constraints

Reverse exchanges impose a liquidity burden that exceeds forward exchanges by an order of magnitude. You must fund the replacement property acquisition in full while simultaneously carrying the relinquished asset, creating a capital bridge that lasts until the relinquished property sells and the exchange closes.

Financing the replacement property during the parking period is structurally difficult. The EAT will appear as borrower on any loan, yet most conventional lenders refuse to underwrite a single-purpose LLC with no operating history, no standalone creditworthiness, and a 180-day sunset clause embedded in its formation documents. Reverse exchange financing therefore defaults to one of three paths:

- All-cash acquisition by the EAT, refinanced post-exchange. You wire sufficient funds for the EAT to close without debt, then refinance in your own name after the exchange completes and you take title. This path delivers clean title and rapid closing but immobilizes substantial capital for up to six months.

- Bridge loan or securities-based line of credit in your name. You borrow against liquid securities, unencumbered investment real estate, or business equity to fund the EAT's cash purchase, then repay the bridge facility with proceeds from the relinquished property sale once it closes.

- Specialized reverse exchange lender. A narrow set of portfolio lenders and private debt funds will lend directly to the EAT, typically at elevated rates and conservative loan-to-value ratios that reflect the short-term maturity and the lender's reliance on your personal guarantee rather than the EAT's nonexistent balance sheet. Terms generally run six to twelve months.

For a coastal replacement property acquisition in the upper price bands, an all-cash parking arrangement can require the investor to deploy millions in liquid capital while simultaneously servicing debt on the relinquished property if it carries a mortgage. This represents a material liquidity test even for portfolios with substantial net worth.

Reverse exchanges are capital-intensive by design. The investors who succeed are those who model the bridge period as a cost of competitive advantage, not a financing inconvenience.

Timeline and Critical Deadlines

The 45-day identification window and 180-day total deadline create compressed timelines for selling the relinquished property.

View chart data

| Category | Days from start |

|---|---|

| EAT Takes Title | 0 |

| Identification Deadline | 45 |

| Remaining Sale Period | 135 |

| Exchange Completion | 180 |

The clock starts when the EAT records title to the parked property. From that date, you have 180 calendar days to complete the entire transaction: sell the relinquished property, transfer proceeds to the QI, and exchange into the replacement property currently held by the EAT.

You must file written identification of the relinquished and replacement properties within 45 days of the EAT's acquisition. This filing is irrevocable. If you fail to sell the relinquished property within the 180-day period, the exchange collapses, the EAT conveys the replacement property to you in a taxable transfer, and you recognize gain on the eventual sale of the relinquished property with no deferral available.

Forward exchanges place pressure on the identification phase (finding replacement property within 45 days); reverse exchanges shift the entire burden to the disposition phase. You must price, market, negotiate, and close the relinquished property within a fixed window, often in a market where you cannot control buyer financing delays, inspection objections, or appraisal disputes.

Strategic Timing Considerations

Experienced coastal operators use reverse exchanges to separate acquisition timing from disposition timing, but they do not ignore sale risk. Best practice is to have the relinquished property already marketed or under contract before you initiate the reverse structure. Acquiring the replacement property on day zero and still searching for a buyer on day 120 leaves you with a 60-day runway to close, often forcing price reductions, buyer concessions, or acceptance of weaker terms to preserve the exchange.

In practice, most successful reverse exchanges in the coastal single-family rental segment close the relinquished property sale within 90 to 120 days of the EAT's replacement acquisition, preserving a buffer for title issues, financing delays, or late-stage renegotiation. Investors who wait until late in the 180-day window to secure a contract routinely miss the deadline, triggering taxable recognition and forfeiting the deferral benefit that justified the structure in the first place.

Coastal Market Applications: When Reverse Exchanges Make Sense

Reverse 1031 exchanges are not appropriate for every transaction. They are a precision instrument for specific market conditions and investor circumstances. In coastal California, four scenarios account for the majority of reverse exchange activity among luxury rental portfolios.

Scenario One: Scarce Beachfront and Ocean-View Inventory

Luxury beachfront single-family rentals in Corona del Mar, La Jolla Shores, Manhattan Beach, and Encinitas trade infrequently. When a premium oceanfront property enters the market, it typically attracts multiple offers within days. Sellers expect all-cash bids, abbreviated escrow periods, and minimal contingencies.

An investor holding a relinquished property in an inland submarket cannot afford to wait 45 days to identify a beachfront replacement, then cross fingers that it remains available while the relinquished property closes escrow. A reverse exchange permits the investor to submit a competitive all-cash offer (via the EAT), close within two weeks, and then market the relinquished property without the forward-exchange identification clock ticking.

Coastal luxury single-family rental inventory in premium price tiers remains below historical norms. Median days on market for oceanfront properties runs materially shorter than for comparable inland luxury homes. In this environment, reverse exchanges are not exotic structures; they are standard tools for serious buyers.Scenario Two: Off-Market and Pocket Listing Opportunities

A substantial share of coastal luxury transactions occur off-market, brokered through long-standing relationships among listing agents, private wealth advisors, and repeat investor clients. These opportunities do not wait for your relinquished property to close. If a broker calls with an off-market deal and you need 90 days to sell your existing asset, the property will trade to another buyer before you can act.

Reverse exchanges allow you to execute immediately on off-market opportunities, locking in the replacement property while you conduct a deliberate, optimized sale of the relinquished asset. This is particularly valuable when the relinquished property is tenant-occupied and you prefer to time the sale to coincide with lease expiration, avoiding the valuation haircut that occupied luxury rentals sometimes face relative to vacant, show-ready comparables.

Scenario Three: Value-Add Replacement Properties Requiring Immediate Work

Coastal investors frequently target dated luxury properties with value-add potential: a 1970s oceanfront home requiring full interior gut-renovation, or a hillside view property with deferred maintenance and obsolete mechanical systems. Acquiring such a property in a forward exchange costs you months of the value-add timeline while you wait for the relinquished property to close and the exchange to complete.

A reverse exchange lets you acquire the replacement property, commence design work, pull permits, and begin construction immediately, completing the renovation while the relinquished property sale progresses in parallel. By the time the exchange closes and you take direct title, the property is rent-ready, allowing you to capture peak-season rental demand without delay. In coastal markets where short-term rental rates for renovated beachfront homes can exceed inland comparables by substantial margins, a six-month head start on construction can generate meaningful incremental first-year NOI.

Scenario Four: Portfolio Rebalancing Across Coastal Submarkets

Sophisticated coastal investors use reverse exchanges to rebalance geographic and asset-class exposure within their portfolios. An investor holding multiple inland properties may seek to consolidate into fewer beachfront assets in premium coastal locations, improving long-term rent growth trajectory and appreciation potential relative to inland alternatives.

Executing this rebalancing via forward exchange requires selling all relinquished properties within a compressed window, then identifying and closing on replacement properties within 180 days, a logistical challenge that often forces suboptimal pricing or acceptance of inferior replacement assets. A reverse exchange allows the investor to acquire the first replacement property when the right opportunity surfaces, then methodically sell the relinquished properties over subsequent months, optimizing sale price and timing for each asset individually rather than executing a forced liquidation to meet an arbitrary deadline.

Tax Compliance and Safe-Harbor Requirements

Revenue Procedure 2000-37 provides a safe harbor, not a mandate. You may structure a reverse exchange outside the safe harbor, but you assume the risk that the IRS will challenge the transaction and deny deferral. Staying within the safe harbor requires strict adherence to five core requirements.

First, the EAT must be a person (an entity) that is neither the taxpayer nor a disqualified person, and it must hold qualified indicia of ownership (legal title recorded in the public land records) at all times during the parking period. Second, the parking period cannot exceed 180 days. Third, you must identify the relinquished and replacement properties in writing within 45 days of the EAT's acquisition of the parked property. Fourth, the combined duration of the parking arrangement and the subsequent exchange cannot exceed 180 days from the EAT's initial acquisition. Fifth, the property must be held for investment or business use under Section 1031, not for personal use or as dealer inventory subject to ordinary income treatment.

The safe harbor also requires the EAT to hold the property consistent with normal commercial practices. This means the EAT should obtain a separate federal tax identification number, maintain separate books and records, and file its own tax returns (typically as a disregarded entity for income tax purposes but with separate informational filings). The EAT should not commingle funds with your personal or business accounts, and all expenses related to the parked property should flow through the EAT's bank account, even though you bear the economic burden of those expenses.

Failure to comply with safe-harbor requirements does not automatically disqualify the exchange, but it shifts the burden to you to demonstrate that the transaction satisfies the general requirements of Section 1031 under a facts-and-circumstances analysis, a significantly higher evidentiary bar and a litigation risk most investors prefer to avoid.

Cost Analysis: Fees, Carrying Costs, and Break-Even Thresholds

Opportunity cost of capital and financing typically dwarf direct QI and legal fees in reverse exchange transactions.

View chart data

| Category | Relative cost impact |

|---|---|

| QI Setup & Monthly Fees | 15 |

| Legal Documentation | 10 |

| Title Insurance | 8 |

| Financing/Bridge Debt Cost | 35 |

| Opportunity Cost of Capital | 32 |

Reverse exchanges carry higher costs than forward exchanges, both in direct fees and in opportunity cost of deployed capital. A complete cost analysis for a coastal replacement property in the upper price bands typically includes the following components:

- QI reverse exchange setup fee: Varies by intermediary and transaction complexity

- Monthly EAT holding fee: Charged for each month or partial month during the parking period

- Legal documentation (EAT formation, parking agreement, exchange agreement): Varies by jurisdiction and complexity

- Title insurance for EAT acquisition and subsequent exchange: Varies by county and property value

- Financing cost (if using bridge debt or specialized reverse lender): Depends on loan structure, principal amount, interest rate, and term

- Opportunity cost of capital: If you deploy substantial liquid capital for several months, you forgo returns on alternative uses of those funds (securities, other real estate, business investment)

Total costs for a typical coastal reverse exchange vary based on transaction size, financing structure, and actual holding period. The break-even question is direct: does the ability to acquire the replacement property now, rather than waiting or losing the opportunity, justify these incremental costs? In a market where luxury coastal inventory is scarce and rent growth is material, the answer is often affirmative. Missing a premium beachfront property that appreciates materially over the 12 to 18 months you spend searching for an alternative can represent foregone equity that dwarfs the reverse exchange fees by an order of magnitude.

Common Pitfalls and How to Avoid Them

Reverse exchanges fail for predictable reasons. The most common error is underestimating the relinquished property sale timeline. Investors acquire the replacement property on day one, assume the relinquished property will sell promptly, and discover themselves on day 140 with no executed contract and no contingency plan. The remedy is to pre-market the relinquished property aggressively, secure a backup buyer willing to close quickly, or price the property to move within a compressed timeframe that preserves a meaningful buffer before the 180-day deadline.

The second common failure is inadequate liquidity planning. Investors structure reverse exchanges assuming they can obtain conventional financing for the replacement property, only to learn that lenders will not underwrite the EAT. By the time they pivot to an all-cash acquisition or arrange bridge financing, they have consumed weeks of the 180-day window and face compressed timelines on both the acquisition and disposition sides of the transaction.

A third error is misunderstanding the identification requirement. In a forward exchange, you identify replacement properties; in a reverse exchange, you identify the relinquished property (the asset you intend to sell). If you own multiple properties and fail to identify the correct relinquished property within 45 days, or if you later attempt to substitute a different property as the relinquished asset, the exchange fails and the deferral is lost.

Finally, investors occasionally violate safe-harbor rules by taking title to the replacement property in their own name before the exchange completes, or by directing the EAT to convey the property to them outside the formal exchange process documented by the QI. Any deviation from the safe-harbor structure, regardless of intent or materiality, can disqualify the entire transaction and trigger immediate taxable recognition.

Strategic Integration with Coastal Portfolio Management

Reverse 1031 exchanges are not standalone transactions; they are portfolio management instruments. The most sophisticated coastal investors integrate reverse exchange capability into their annual acquisition and disposition planning, maintaining liquidity reserves and lender relationships specifically to enable opportunistic acquisitions when the right replacement property surfaces.

This requires running a rolling 12-month acquisition pipeline, tracking off-market opportunities, maintaining relationships with brokers who specialize in luxury coastal listings, and pre-qualifying for bridge financing or reverse exchange lender programs before you identify a specific property. It also requires stress-testing your relinquished property sale assumptions by modeling potential price adjustments, extended listing periods, or buyer financing failures to confirm you can still close within the 180-day window if market conditions deteriorate or an unexpected issue surfaces during due diligence.

For investors managing substantial coastal rental portfolios distributed across multiple submarkets, reverse exchange capability represents a competitive advantage. It permits you to act on the best opportunities when they appear, rather than waiting for your existing assets to sell. In markets where premium coastal properties deliver higher rent growth and superior long-term appreciation than inland alternatives, the ability to upgrade into superior assets without timing constraints can compound to material portfolio performance differences over a multi-year hold period.

The investors who built dominant coastal portfolios in the 2010s were the ones who could move when opportunity appeared, not the ones who waited for perfect timing.

Reverse vs. Forward: Choosing the Right Structure

Not every exchange should be structured as a reverse exchange. Forward exchanges remain the default for most transactions; they are simpler, less expensive, and less capital-intensive. The decision framework is straightforward.

Choose a forward exchange when: (1) you have reasonable confidence you can identify suitable replacement property within 45 days, (2) the replacement property market exhibits adequate inventory and normal days-on-market metrics, (3) you do not face competitive bidding pressure that demands all-cash offers or abbreviated escrow periods, and (4) you prefer to minimize upfront capital deployment and incremental exchange fees.

Choose a reverse exchange when: (1) you have identified a specific replacement property that will not remain available while your relinquished property sells, (2) you are competing in a supply-constrained market where inventory turns rapidly, (3) you are pursuing an off-market or pocket listing opportunity that requires immediate execution, (4) the replacement property requires immediate construction or value-add work that you want to commence before the exchange closes, or (5) you seek to decouple acquisition timing from disposition timing to optimize pricing and terms on both ends of the transaction.

In coastal California's luxury single-family rental market, the calculus increasingly favors reverse structures. Inventory in premium beachfront segments remains below historical averages, median days on market for top-tier properties is compressed relative to inland comparables, and the share of all-cash offers in luxury transactions is elevated. In this environment, the ability to close quickly and compete with cash buyers often determines whether you acquire a generational asset or watch it trade to a better-capitalized competitor.

How NextGen Coastal Supports Reverse Exchange Investors

Reverse 1031 exchanges require flawless execution across multiple operational workstreams: property management continuity during the parking period, tenant communication if the relinquished property is occupied, coordination with QIs and title companies on document execution and For investors building a multi-strategy California portfolio, sister brand Dwell by NextGen runs a complementary rent-to-own program and build-to-rent communities targeting entry-level buyers, useful where coastal luxury yields meet a different demand profile. fund transfers, and financial reporting that segregates EAT activity from your personal books. We manage these details for coastal investors executing complex exchange strategies.

Our team coordinates with your qualified intermediary to confirm the EAT receives all rental income, remits all operating expenses, and maintains separate accounting records throughout the parking period. We handle tenant notifications, lease assignments to and from the EAT, and vendor transitions so that property operations continue without interruption while title resides temporarily with the EAT. And we provide the financial transparency and documentation your CPA requires to substantiate safe-harbor compliance and support your tax filings at year-end.

For investors managing substantial coastal portfolios across multiple submarkets, this operational support is not a convenience; it is a prerequisite. A single missed rent payment deposited to the wrong account, a commingled expense paid from your personal funds, or a documentation gap in the EAT's books can jeopardize safe-harbor status and expose the entire transaction to IRS challenge. NextGen Coastal's platform produces exchange-compliant accounting, reporting, and documentation from day one, eliminating execution risk and allowing you to focus on the strategic aspects of the transaction rather than the administrative mechanics.

Frequently Asked Questions

What is the main difference between a reverse 1031 exchange and a forward 1031 exchange?

How much does a reverse 1031 exchange cost?

Can I get a mortgage for the replacement property in a reverse 1031 exchange?

What happens if I can't sell the relinquished property within 180 days?

When does a reverse 1031 exchange make sense for coastal California investors?