What AB 1033 Authorizes, and What It Does Not

On January 1, 2024, AB 1033 amended Government Code § 65852.26 to permit local agencies to adopt ordinances authorizing separate conveyance of ADUs as condominiums, contingent on the ADU's compliance with state ADU law. The statute removes the prohibition; it does not compel adoption. Each city council or county board of supervisors must pass an affirmative ordinance, and that ordinance may layer in additional restrictions: owner-occupancy mandates, per-parcel unit caps, affordability covenants, design overlays.

Interactive Tool

AB 1033 ADU Sale vs. Rental Hold Calculator

Compare after-tax proceeds from condo sale against long-term rental NOI

Hard cost + soft cost + permits

Legal, survey, reserve study

Commission + title + escrow (typically 6.5%)

Federal + state (e.g. 15% + 9.3% = 24.3%)

Property tax, insurance, maintenance, vacancy, management

Original purchase price + improvements

The legal mechanism requires that both the ADU and the primary dwelling be organized as a common-interest development under the Davis-Stirling Common Interest Development Act (Civil Code § 4000 et seq.). The selling owner becomes the declarant of a two-unit (or larger, if multiple ADUs are present) condominium regime. You must file a declaration of covenants, conditions, and restrictions; a condominium plan; and you must establish an HOA with a reserve study and operating budget. This is not a lot split. It is a full CID creation, with the administrative and financial overhead that goes with it.

AB 1033 does not preempt local zoning, design review, or coastal permitting. The ADU must have been legally permitted under state ADU law (Gov. Code § 65852.2 or § 65852.22). In the Coastal Zone, the city's AB 1033 ordinance must conform to the certified Local Coastal Program, and the California Coastal Commission reviews the underlying ADU permit for coastal-development compliance. The condo-conversion act itself is administrative; it does not trigger a new CDP unless the LCP explicitly demands one.

Only 9 of 17 tracked coastal and near-coastal cities have adopted enabling ordinances as of Q2 2026, with Southern California jurisdictions lagging Bay Area adoption.

City Opt-In Landscape: Who Has Adopted, Who Is Resisting

View chart data

| Category | Adoption Status (1=Active, 0.5=Under Study, 0=No Ordinance) |

|---|---|

| Berkeley | 1 |

| Oakland | 1 |

| Santa Cruz | 1 |

| San Diego | 1 |

| San Jose | 1 |

| Sacramento | 1 |

| San Francisco | 1 |

| Carlsbad | 1 |

| Los Angeles | 1 |

| Long Beach | 1 |

| Encinitas | 1 |

| Pasadena | 0 |

| Santa Monica | 0 |

| Malibu | 0 |

| Newport Beach | 0 |

| Laguna Beach | 0 |

| Costa Mesa | 0 |

As of Q2 2026, fewer than two dozen California cities have adopted AB 1033 enabling ordinances. Coastal-zone jurisdictions that have opted in cluster in the Bay Area and San Diego County. The table below summarizes the status in key cities within our coastal service area and adjacent inland markets.

| City | Ordinance | Effective Date | Max ADUs per Parcel | HOA Required | Status |

|---|---|---|---|---|---|

| Berkeley | Ord. 7,785-N.S. | March 2024 | 2 | Yes | Active |

| Oakland | Ord. 13,692 | June 2024 | 2 | Yes | Active |

| Santa Cruz | Ord. 2024-08 | August 2024 | 1 | Yes | Active |

| San Diego | Ord. O-21,987 | January 2025 | 3 | Yes | Active |

| San Jose | Ord. 30,845 | November 2024 | 2 | Yes | Active |

| Sacramento | Ord. 2024-0032 | July 2024 | 2 | Yes | Active |

| Los Angeles | , | , | , | , | Under study [VERIFY] |

| Long Beach | , | , | , | , | Under study [VERIFY] |

| San Francisco | Ord. 45-25 | February 2025 | 1 | Yes | Active |

| Pasadena | , | , | , | , | No ordinance |

| Santa Monica | , | , | , | , | No ordinance |

| Malibu | , | , | , | , | No ordinance |

| Carlsbad | Ord. CS-422 | March 2025 | 1 | Yes | Active |

| Encinitas | , | , | , | , | Under study [VERIFY] |

| Newport Beach | , | , | , | , | Publicly opposed |

| Laguna Beach | , | , | , | , | Publicly opposed |

| Costa Mesa | , | , | , | , | No ordinance [VERIFY] |

Both Newport Beach and Laguna Beach city councils have signaled resistance. Parking, neighborhood character, and the administrative burden of enforcing two-unit HOAs top the list of stated concerns. Los Angeles and Long Beach are conducting feasibility studies; neither has brought an ordinance to a vote. For an investor planning a build-and-sell strategy, the city must have an active ordinance before construction begins. Building the ADU in anticipation of future opt-in is the single most common failure mode we observe.

The Davis-Stirling HOA Requirement: What You Must File

Under AB 1033, separate sale of the ADU requires creation of a common-interest development governed by the Davis-Stirling Act. This is mandatory. The declarant (the original owner) must prepare and record the following documents:

- A Declaration of Covenants, Conditions, and Restrictions that defines common area (typically the land beneath both structures, shared utilities, driveways, landscaping), exclusive-use areas (the interior of each unit), and the allocation of common expenses.

- A condominium plan or survey map depicting the legal boundaries of each unit in three dimensions, prepared by a licensed surveyor or civil engineer.

- An HOA operating budget and a reserve study projecting 30-year capital expenditures for roof, foundation, exterior paint, shared systems, and landscaping. Civil Code § 5550 requires a reserve study for any HOA, even a two-unit association.

- Articles of incorporation and bylaws for the homeowners association, typically a California nonprofit mutual benefit corporation.

Professional preparation of these documents costs between $8,000 and $15,000 in legal and engineering fees for a simple two-unit ADU conversion, according to our experience with recent projects in Oakland and San Diego. The reserve study alone costs $2,500 to $4,000. Once the HOA is formed, the two owners (the seller of the ADU and the buyer) share monthly HOA dues to fund reserves and common-area maintenance. For a modest single-family home plus detached ADU, monthly dues typically start at $150 to $250 per unit, rising over time as the reserve study dictates.

The Davis-Stirling framework was designed for 50-unit condo towers, not two-unit SFR-plus-ADU parcels. The administrative overhead is identical, and the per-unit cost is punishing at small scale.

Financing Reality: Non-QM, Portfolio, and Cash Buyers

As of mid-2026, neither Fannie Mae nor Freddie Mac has issued guidance classifying AB 1033 ADU condos as warrantable. Without that designation, conventional lenders will not offer conforming 30-year fixed mortgages to ADU-condo buyers. The first wave of sales draws from three buyer pools:

- Cash buyers: investors or owner-occupants who can close without financing. In coastal markets this represents 30 to 40 percent of all transactions.

- Portfolio lenders: local banks and credit unions that hold loans on their own balance sheet. Rates run 6.5 to 8.0 percent, and the lender will require a full appraisal, title policy, and HOA review.

- Non-QM lenders: specialty mortgage companies offering non-qualified-mortgage products at 7.5 to 9.5 percent with 20 to 30 percent down. These loans are not sold to Fannie or Freddie and carry higher servicing costs.

For the seller, this financing constraint compresses the buyer pool and may depress the sale price by 5 to 10 percent relative to a warrantable condo. For the buyer, the higher rate and down-payment requirement mean that the ADU-condo must pencil at a significantly lower price per square foot than a comparable detached single-family home to deliver equivalent monthly payment affordability.

We expect Fannie and Freddie guidance by late 2026 or early 2027. At that point the market will open to conventional buyers and pricing will normalize. Early sellers are effectively paying a liquidity discount.

Subdivision Map Act Compliance: Condo Plan vs. Parcel Map

AB 1033 explicitly states that separate conveyance of an ADU does not constitute a subdivision of land under the Subdivision Map Act (Gov. Code § 66410 et seq.), provided the conveyance is accomplished through a condominium plan recorded pursuant to Civil Code § 4285. This distinction matters. The owner does not file a Tentative Parcel Map or Final Map with the city. The owner does not pay subdivision fees. The owner does not trigger CEQA review for a land division.

The condominium plan itself must be prepared by a licensed professional and must comply with the survey and monumentation standards in Civil Code § 4285. It depicts the three-dimensional boundaries of each unit (floor, ceiling, walls) and the common area. It must be recorded in the county recorder's office along with the CC&Rs. The city planning department reviews the plan for consistency with the AB 1033 ordinance but does not treat it as a subdivision application.

If the owner attempts to create separate legal parcels (APNs) without a condominium plan, by filing a lot-line adjustment or a two-lot minor subdivision for example, the city will require full Subdivision Map Act compliance. That includes tentative and final maps, improvement agreements, and CEQA. The condo-plan path is the only streamlined route authorized by AB 1033.

Property-Tax Treatment: New APN, Separate Assessed Value, Prop 13 Basis

When the ADU is sold as a condo, the county assessor assigns a new Assessor's Parcel Number to the ADU unit and a separate APN to the primary dwelling. Each unit receives its own assessed value. Each owner receives a separate property-tax bill. The ADU's assessed value is established at the sale price (the change-in-ownership event). The primary dwelling's assessed value remains at its existing Prop 13 factored base year value, unchanged by the ADU sale.

For the seller, this means the ADU sale does not trigger reassessment of the primary dwelling. The seller retains the Prop 13 basis on the main house. Only the ADU is assessed at market value in the hands of the new owner. For the buyer, the ADU's assessed value starts at the purchase price; annual increases are capped at 2 percent under Prop 13 until the next change in ownership.

If the seller originally constructed the ADU while owning the primary dwelling, the construction cost was added to the primary dwelling's assessed value as new construction under Revenue and Taxation Code § 70. When the ADU is later sold as a condo, the assessor removes that increment from the primary dwelling's roll value and establishes it as the ADU's new base year value at the sale price. The net result is that the combined assessed value of the two units post-sale may be higher or lower than the pre-sale single-parcel value, depending on the sale price relative to the construction cost.

AB 1482 Rent Control Interaction: Does the New Owner Get the Exemption?

Once the ADU is sold as a separate condo, it is owned by a different legal entity than the primary dwelling. If the new ADU owner qualifies for an exemption under AB 1482 (the California Tenant Protection Act), the ADU is exempt from the 5 percent plus CPI annual rent-increase cap and the just-cause eviction requirements. The most common exemptions are:

- Single-family home exemption (Civil Code § 1946.2(e)(2)(A)): the ADU is a detached single-family residence, and the owner is a natural person (not a corporation, LLC, or REIT). This exemption sunsets if the property is later sold to a corporate entity.

- Duplex exemption (Civil Code § 1946.2(e)(2)(B)): the owner occupies one of the two units as a primary residence. If the ADU buyer lives in the ADU and rents out the primary dwelling (or vice versa), the exemption applies.

If the new ADU owner is a corporate entity or does not occupy either unit, AB 1482 applies in full. The ADU is subject to rent control and just-cause eviction. The seller of the ADU (who retains the primary dwelling) must separately evaluate whether the primary dwelling remains exempt. If the seller is a natural person and the primary dwelling is a single-family home, the exemption continues.

For investors, this creates a planning opportunity. Selling the ADU to an owner-occupant buyer preserves the duplex exemption for that buyer. The seller retains the single-family exemption on the primary dwelling. Both units remain outside AB 1482, maximizing rent-setting flexibility.

Coastal Zone Overlay: CCC Review and LCP Conformance

In the Coastal Zone, the city's AB 1033 ordinance must be consistent with the certified Local Coastal Program. The underlying ADU permit must have been issued in compliance with the Coastal Act. The California Coastal Commission does not review the condo-conversion act itself. Recordation of the CC&Rs and condominium plan is administrative. But the CCC does review the ADU permit for coastal-development compliance.

If the ADU was permitted under a categorical exemption or a local CDP, the condo conversion proceeds without additional CCC involvement. If the ADU required a CCC-issued CDP (because the city's LCP does not cover ADUs, or the ADU is in the appeals jurisdiction), the CDP conditions travel with the property and bind the new ADU owner. Common CDP conditions that affect AB 1033 sales include:

- Short-term rental prohibition: the CDP may prohibit vacation rentals of the ADU. That restriction runs with the land, binding the buyer.

- Deed restriction requiring long-term rental: some CDPs condition ADU approval on a recorded covenant that the ADU be rented at affordable rates for 10 to 20 years. If such a restriction exists, the ADU cannot be sold as a market-rate condo until the restriction expires or is released by the CCC.

- Sea-level-rise adaptation: in low-lying coastal areas, the CDP may require the ADU to be elevated, set back from a bluff edge, or designed for future relocation. These conditions increase construction cost and may spook lenders or buyers concerned about long-term habitability.

Newport Beach and Laguna Beach have both cited coastal-zone constraints as a reason for declining to adopt AB 1033 ordinances. In these cities, the combination of restrictive LCPs, high CCC scrutiny, and vocal neighborhood opposition has stalled any movement toward ADU condo sales. San Diego, by contrast, adopted an AB 1033 ordinance that explicitly cross-references the city's certified LCP and requires that any ADU sold as a condo have a valid CDP or categorical exemption on file.

Worked Example: Costa Mesa SFR + Detached ADU Build-and-Sell

The build-and-sell strategy delivers 75% one-time return versus 4% annual unlevered yield, favoring sale for liquidity-focused investors.

View chart data

| Category | Return on Investment |

|---|---|

| Sale Return (18-mo) | 0.8% |

| Rental CoC (Annual, Unlevered) | 0.0% |

Assume Costa Mesa adopts an AB 1033 ordinance in Q4 2026. An investor owns a single-family home purchased in 2022 for $950,000, with a current assessed value of $970,000 (Prop 13 factored basis). In early 2027 the investor builds a detached 1,000-square-foot ADU at an all-in cost of $325,000 (hard cost $275,000, soft cost $50,000). The ADU is completed and rented at $3,200 per month while the investor waits for the AB 1033 ordinance to take effect.

Once the ordinance is active, the investor engages an attorney to prepare the CC&Rs, condominium plan, and HOA formation documents at a cost of $12,000. A reserve study is commissioned for $3,500. The investor lists the ADU for sale at $725,000 in mid-2027 and closes escrow 60 days later with a cash buyer. Sale proceeds break down as follows:

- Sale price: $725,000

- Closing costs (6 percent commission plus title and escrow): $47,250

- Net proceeds: $677,750

The investor's basis in the ADU is the original construction cost of $325,000 plus the HOA formation cost of $15,500, for a total basis of $340,500. Capital gain is $677,750 minus $340,500 equals $337,250. If the investor held the property for more than one year, the gain is long-term and taxed at 15 percent federal (for most investors) plus 9.3 percent California, for a combined rate of 24.3 percent. That yields a tax liability of $81,952. After-tax net proceeds are $595,798.

The investor's all-in cash outlay was $340,500. After-tax profit is $595,798 minus $340,500 equals $255,298, a 75 percent return on the construction investment over an approximately 18-month hold (12 months construction plus permitting, six months rental holding period to establish long-term gain).

Alternative scenario: the investor holds both the primary dwelling and the ADU as rentals. Primary dwelling rents for $3,800 per month. ADU rents for $3,200 per month. Combined gross rent is $7,000 per month, or $84,000 per year. At a 40 percent operating-expense ratio (property tax, insurance, maintenance, vacancy, management), NOI is $50,400. The investor's basis in the combined property is $950,000 (primary) plus $325,000 (ADU), equals $1,275,000. Cash-on-cash return is 3.95 percent if the property is owned free and clear, or a levered return of 8 to 12 percent if financed at 60 percent LTV.

The build-and-sell strategy delivers a faster, larger cash return but eliminates the ongoing income stream and the long-term appreciation. Hold-as-rental delivers lower immediate return but preserves the asset for future appreciation and potential 1031 exchange. For an investor with a five- to seven-year horizon, the rental hold is typically superior. For an investor seeking liquidity or redeployment into a larger project, the AB 1033 sale is compelling.

Common Failure Modes: What Trips Investors

We see five recurring mistakes in AB 1033 planning:

- Building before the city opts in. Constructing the ADU in 2025 with the assumption that the city will adopt an AB 1033 ordinance by 2027, only to discover that the city declines or delays indefinitely. The investor is stuck with a rental-only asset and cannot recoup the construction cost through a sale. Mitigation: do not break ground until the ordinance is adopted and effective.

- Skipping the reserve study. Filing the CC&Rs and condominium plan without commissioning a reserve study, in violation of Civil Code § 5550. The buyer's lender (if any) will catch this in the HOA review and refuse to fund. The title company may also refuse to insure. Mitigation: budget for a reserve study and include it in the HOA formation package.

- Financing the ADU with a non-condo-eligible HELOC. Taking a home-equity line of credit against the primary dwelling to fund ADU construction, then discovering that the HELOC lender will not subordinate or release the lien on the ADU parcel when it is sold as a condo. The investor cannot deliver clear title to the buyer. Mitigation: before drawing on the HELOC, confirm in writing that the lender will execute a partial release or subordination agreement for the ADU parcel.

- Ignoring an existing HOA prohibition. The primary dwelling is already part of a master-planned community HOA that prohibits subdivision or separate sale of any portion of the lot. The investor builds the ADU, then learns that the master HOA will not approve the condo conversion. Mitigation: review the master CC&Rs before designing the ADU; if subdivision is prohibited, AB 1033 is not viable.

- Coastal-zone short-term-rental conflict. The ADU CDP includes a condition prohibiting vacation rentals, but the investor markets the ADU-condo to a buyer who intends to Airbnb it. The buyer discovers the restriction post-close and sues for rescission or damages. Mitigation: disclose all CDP conditions in the purchase agreement and require the buyer to acknowledge them in writing.

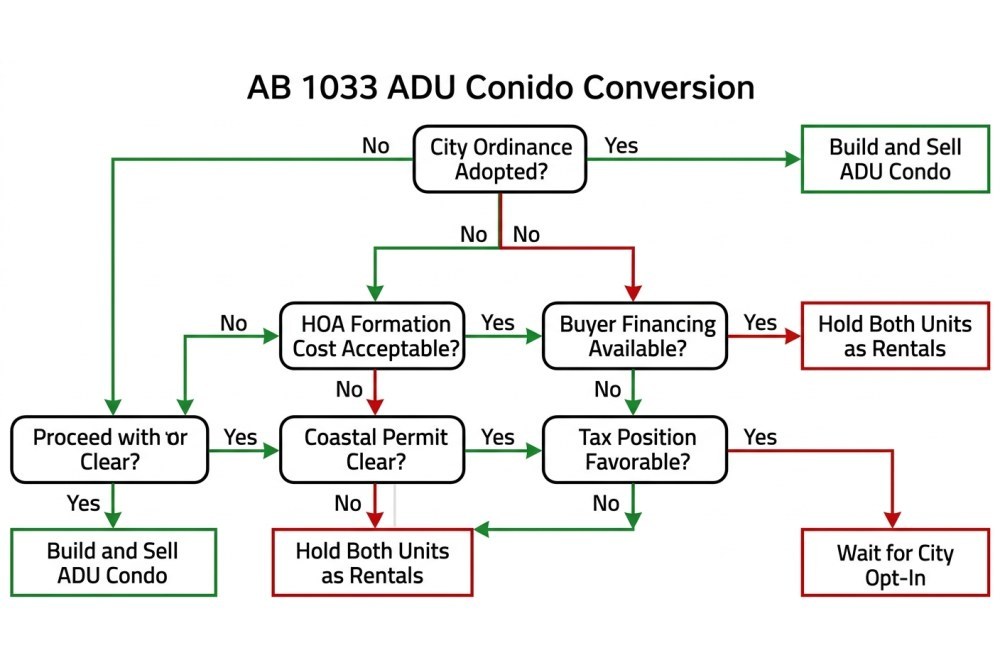

Go / No-Go Decision Matrix

Use this matrix to evaluate whether AB 1033 condo conversion makes sense for your coastal California ADU project:

| Factor | Green Light (Proceed) | Red Light (Hold as Rental) |

|---|---|---|

| City ordinance | Adopted, effective, no sunset clause | Under study, opposed, or no ordinance |

| Construction timeline | ADU completed after ordinance effective date | ADU completed before ordinance, or construction not yet started |

| Financing | Cash construction, or HELOC with confirmed partial-release agreement | HELOC without subordination, or construction loan that clouds title |

| Existing HOA | No master HOA, or master CC&Rs allow subdivision | Master HOA prohibits subdivision or separate sale |

| Coastal permits | Valid CDP or categorical exemption, no rental restrictions | CDP with affordability covenant, STR ban, or sea-level-rise relocation requirement |

| Buyer pool | Strong cash-buyer market, or portfolio lenders active in the area | Weak cash market, no local portfolio lenders, Fannie/Freddie guidance still pending |

| Hold period | Investor needs liquidity within 12 to 24 months | Investor has 5+ year horizon and values income stream |

| Tax position | Investor in low tax bracket, or can harvest capital loss to offset gain | Investor in high bracket (37 percent federal plus 13.3 percent CA), or no offsetting losses |

If you score green on six or more factors, AB 1033 is worth modeling. If you score red on three or more factors, hold-as-rental is safer and likely more profitable measured on a five- to seven-year horizon.

How NextGen Coastal Supports AB 1033 Investors

Our coastal team has managed ADU rentals since 2019. We are now advising clients on AB 1033 condo-conversion feasibility as cities adopt enabling ordinances. We provide:

- City ordinance tracking. We monitor every coastal and near-coastal jurisdiction for AB 1033 adoption, effective dates, and amendment activity. We alert clients when their target city opts in.

- HOA formation coordination. We connect clients with experienced real-estate attorneys who specialize in small-scale CID creation. We review the CC&Rs and reserve study for operational feasibility before recordation.

- Rental bridge management. If you build the ADU before the city opts in, we lease and manage both units as rentals during the hold period, maximizing NOI while you wait for the ordinance to take effect.

- Sale-leaseback structuring. For clients who want to sell the ADU but retain occupancy of the primary dwelling, we structure sale-leaseback agreements that allow the ADU buyer to rent the primary dwelling back to the seller at market rate, preserving the seller's residence while liquidating ADU equity.

- 1031 exchange planning. If you sell the ADU as investment property (not primary residence), we coordinate with qualified intermediaries to structure the sale as part of a 1031 exchange into a larger coastal rental portfolio.

We do not provide legal or tax advice. We work alongside your attorney, CPA, and lender to structure the AB 1033 transaction correctly from day one. Our 5.9 percent management fee applies to rental income during the hold period; we do not charge transaction fees on ADU sales.

Frequently Asked Questions

Can I sell my ADU separately if my city has not adopted an AB 1033 ordinance?

Do I need to create an HOA even if I am selling the ADU to a family member?

Will a conventional lender finance the ADU purchase for my buyer?

Does selling the ADU trigger reassessment of my primary dwelling under Prop 13?

If I sell the ADU, does the new owner have to comply with AB 1482 rent control?