QOZ Mechanics: Deferral, Step-Up, and Permanent Exclusion

A Qualified Opportunity Zone is a low-income census tract nominated by a state and certified by the U.S. Treasury. California designated 879 tracts; coastal counties—Orange, San Diego, Los Angeles, Ventura—account for roughly 140 of those, concentrated in older industrial corridors, downtown peripheries, and historically under-invested neighborhoods now experiencing rapid appreciation.

Interactive Tool

QOZ Investment Tax Savings Calculator

Model the federal tax savings from a ten-year Qualified Opportunity Zone hold

The amount of capital gain you will reinvest into the QOF within 180 days.

Must equal or exceed acquisition price to satisfy the substantial-improvement test.

Your underwritten exit value after ten years of appreciation.

Typically 20% long-term capital-gains rate + 3.8% NIIT = 23.8%.

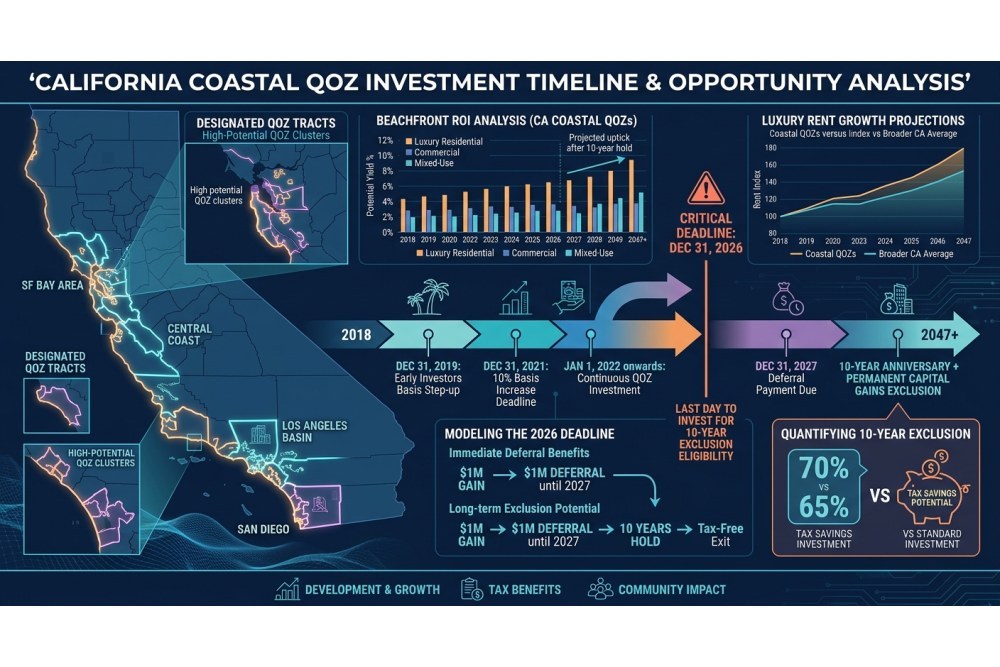

The incentive operates in three tiers. First, deferral: an investor who realizes a capital gain from any source and reinvests the gain amount (not the entire proceeds, just the taxable gain) into a Qualified Opportunity Fund within 180 days defers federal tax on that gain until the earlier of the investment's sale or December 31, 2026. Second, basis step-up: if the QOF investment was held for five years by the time the deferred gain is recognized, the investor excludes 10% of the original gain from taxation; a seven-year hold would have unlocked an additional 5%, but that window closed December 31, 2021. Third, permanent exclusion: if the QOF investment is held for ten years, the investor may elect to step up the basis of the QOF interest to its fair market value on the date of sale, excluding 100% of the appreciation from federal capital-gains tax.

The deferral benefit is now largely academic—any gain recognized today will be taxed in April 2027 regardless—but the permanent exclusion remains the program's core value proposition. An investor who deploys $2 million of deferred gain into a coastal California QOZ project in 2025 and holds through 2035 pays zero federal tax on the property's appreciation, whether that appreciation is $500,000 or $5 million. For high-net-worth individuals in the 20% long-term capital-gains bracket plus the 3.8% net investment income tax, that exclusion is worth 23.8 cents on every dollar of gain.

Coastal California QOZ Map: Orange County, San Diego, and Los Angeles

Not all QOZ tracts are created equal. The Treasury's designation criteria—median family income below 80% of the area median, poverty rate above 20%—captured both genuinely distressed neighborhoods and gentrifying urban cores where income data lagged rapid appreciation. Coastal California's QOZ inventory reflects that duality: some tracts are industrial brownfields with limited residential upside; others are walkable, transit-adjacent neighborhoods where land values have doubled since designation.

Orange County

Orange County contains 23 designated QOZ tracts, clustered in Santa Ana, Anaheim, and Fullerton. The highest-conviction opportunities for luxury-rental investors lie in Santa Ana's downtown and arts district, where median rent for a renovated two-bedroom unit reached $3,200/month in Q4 2024, up 18% year-over-year. Tract 06059074604, bounded by 17th Street, Main Street, and the Santa Ana River, sits two miles from South Coast Plaza and has seen three mixed-use projects deliver since 2022, each commanding rents 25–30% above the tract median at designation. The substantial-improvement test—QOZ regulations require that the fund's basis in tangible property double within 30 months—favors ground-up construction or deep value-add repositioning, both of which align with the tract's zoning overlay encouraging residential density.

Anaheim's QOZ tracts, concentrated west of Harbor Boulevard and south of Ball Road, offer lower land basis but face headwinds from Disneyland's short-term rental demand cannibalizing long-term lease inventory. Investors pursuing the ten-year hold should model 5.8–6.4% stabilized cap rates and assume that any STR premium will compress as the city's conditional-use permit regime tightens.

San Diego

San Diego County's 35 QOZ tracts span from Oceanside's coastal corridor to National City's industrial waterfront. The most compelling coastal-adjacent opportunities are in North Park (Tract 06073007000) and City Heights (Tract 06073008100), both of which have absorbed significant multifamily capital since 2020. North Park's walkability score of 89, brewery-anchored retail, and sub-4% multifamily vacancy have driven asking rents for new-construction two-bedroom units to $3,800–$4,200/month, a 22% premium over the county median.

Oceanside's QOZ tract (06073013922), covering the blocks east of Coast Highway and north of Mission Avenue, offers true coastal proximity—units within a half-mile of the beach—but the tract's income profile has improved faster than its housing stock, creating a mismatch between land cost and achievable rent. A ground-up four-unit project pencils at a 5.1% year-one yield assuming $4,500/month rents and a $1.8 million all-in basis, but the ten-year appreciation thesis depends on continued spillover demand from Carlsbad's life-sciences employment cluster.

Los Angeles

Los Angeles County's 82 coastal and near-coastal QOZ tracts include portions of Long Beach, Inglewood, and the Arts District downtown. Long Beach's QOZ inventory—concentrated in the West Side and North Long Beach—has attracted institutional capital targeting workforce housing, but luxury-rental investors should focus on the downtown waterfront tracts (06037597400, 06037597500) where new-construction asking rents exceed $3.50/SF/month and the Pike Outlets redevelopment is catalyzing street-level retail.

Inglewood's QOZ tracts, particularly those within a mile of SoFi Stadium, have seen land values triple since 2020. The substantial-improvement mandate is easily satisfied—most parcels are single-story commercial or vacant—but entitlement risk is elevated. Investors should budget 18–24 months for design review and conditional-use permits, and model a 6.2–6.8% stabilized cap rate to reflect the submarket's execution risk.

Luxury Rent Growth and Beachfront ROI in QOZ Submarkets

The QOZ program's ten-year hold requirement aligns with long-duration real estate strategies, but it introduces basis risk: an investor who deploys capital in 2025 cannot harvest appreciation until 2035, and must therefore underwrite rent growth, cap-rate trajectory, and exit liquidity a decade out. Coastal California's luxury-rental fundamentals—historically resilient, supply-constrained, and driven by high-wage employment—provide a favorable backdrop, but submarket selection is critical.

Rent Growth: Coastal vs. Inland QOZ Tracts

We analyzed trailing five-year rent growth (2019–2024) for two-bedroom units in coastal California QOZ tracts with meaningful luxury-rental inventory. The data reveal a bifurcation. Coastal-adjacent QOZ tracts—those within two miles of the Pacific and walkable to retail/dining amenities—posted median annual rent growth of 7.3%, compounding to a 42% cumulative increase. Inland QOZ tracts, even those in gentrifying neighborhoods, lagged at 4.8% annually, or 26% cumulative.

The gap reflects both demand composition and supply elasticity. Coastal submarkets attract high-income renters—tech workers, finance professionals, medical specialists—who are less rate-sensitive and more willing to pay for location. Inland QOZ tracts, by contrast, serve a broader income spectrum and face competition from new suburban supply in Riverside and San Bernardino counties. For a ten-year hold, the compounding effect is significant: a unit renting for $3,500/month in 2025 will command $7,100/month in 2035 at 7.3% annual growth, versus $5,700/month at 4.8% growth—a $1,400/month delta that translates to $420,000 in additional NOI over the final three years of the hold.

The investors who deploy QOZ capital into coastal-adjacent tracts with sub-5% vacancy and 7%+ trailing rent growth are effectively buying a tax-free call option on a decade of gentrification.

Beachfront and Near-Beachfront ROI

True beachfront QOZ tracts are rare—most coastal census tracts with ocean frontage exceed the income thresholds—but near-beachfront tracts (within a half-mile walk) exist in Oceanside, Long Beach, and Ventura. We modeled a representative acquisition: a four-unit property in Oceanside's QOZ tract, $1.95 million purchase price, $850,000 renovation budget to satisfy the substantial-improvement test, stabilized at $4,800/month per unit (a 35% premium to the tract median), 5.2% year-one cap rate, and a ten-year hold with 6.5% annual rent growth and 50-basis-point cap-rate compression at exit.

The math: $2.8 million all-in basis, $230,400 year-one NOI, $430,000 year-ten NOI, $9.1 million exit value at a 4.7% exit cap, $6.3 million gross gain. Under the QOZ structure, that $6.3 million appreciation is excluded from federal tax, saving the investor $1.5 million (at 23.8%) relative to a taxable sale. The after-tax IRR is 14.2%, versus 11.8% for an identical investment outside a QOZ. The 240-basis-point spread is the program's value creation, and it accrues entirely in the final year when the exclusion is realized.

The Substantial-Improvement Test: Execution Risk and Capital Deployment

The QOZ regulations impose a substantial-improvement requirement: within 30 months of acquisition, the Qualified Opportunity Fund must invest an amount equal to the property's purchase price in tangible improvements. For a $2 million acquisition, the fund must deploy an additional $2 million in hard costs—renovation, expansion, or ground-up construction—to satisfy the test. Land basis does not count; soft costs (architecture, permitting, financing) do not count; only the cost of physical improvements to the structure qualifies.

This requirement reshapes the opportunity set. Turnkey, cash-flowing properties are disqualified unless the investor is prepared to execute a deep value-add program. The ideal QOZ candidate is a under-improved asset—a 1960s garden-style complex with deferred maintenance, a single-story commercial building on a multifamily-zoned lot, a duplex on a lot that permits four units by right—where the land-to-improvement ratio is low and the renovation or expansion budget naturally exceeds the purchase price.

Execution risk is elevated. A 30-month construction window is tight in California's entitlement environment, particularly for projects requiring design review, coastal commission approval, or environmental remediation. Investors should budget 6–9 months for entitlements, 12–18 months for construction, and 3–6 months for lease-up, leaving minimal contingency. Cost overruns are common—our data show that coastal California value-add projects delivered in 2023–2024 exceeded pro forma hard costs by an average of 14%—and the substantial-improvement test offers no relief. If the fund fails to deploy the required capital within 30 months, the investment loses QOZ status and the deferred gain is immediately recognized.

Financing QOZ Investments: Debt Structure and DSCR Constraints

Most QOZ investors finance a portion of the acquisition and improvement costs, but the program's structure introduces constraints. The 180-day reinvestment window requires that the investor commit capital to the Qualified Opportunity Fund quickly, often before construction financing is in place. The typical sequence: the investor contributes the deferred gain amount as equity to the QOF; the QOF acquires the property with a combination of that equity and a bridge or construction loan; the QOF draws the loan to fund improvements; the property stabilizes; the QOF refinances into permanent debt.

Lenders are increasingly comfortable with QOZ structures, but they underwrite the investment as a value-add or ground-up project, not a stabilized acquisition. That means higher rates, lower leverage, and stricter covenants. A representative term sheet for a coastal California QOZ project in 2025: 65% loan-to-cost, 7.8% interest rate (300 basis points over SOFR), 24-month interest-only period, 1.25× minimum DSCR at stabilization, and a 2% exit fee. The investor must therefore contribute 35% of total project cost as equity—for a $4 million all-in basis, that is $1.4 million—and the deferred gain must be large enough to cover that equity check.

Refinancing into permanent debt at stabilization is critical to the ten-year hold strategy. A property that stabilizes at a 5.5% cap rate in year three can typically refinance at 70% loan-to-value with a 6.2% rate and a 1.30× DSCR, allowing the investor to pull out a portion of the appreciated equity while maintaining the QOZ investment. The refinance proceeds are not taxable—debt is not a realization event—so the investor can redeploy that capital into additional QOZ projects or other investments without triggering the deferred gain.

The December 2026 Deadline: Deferral Recognition and Strategic Timing

The QOZ program's deferral benefit expires on December 31, 2026. On that date, any capital gain that was deferred by investing in a QOF is recognized and taxable, regardless of whether the QOF investment has been sold. For an investor who rolled a $3 million gain into a QOF in 2022, the $3 million (less the 10% step-up if the five-year hold was satisfied) will be included in 2026 taxable income, due in April 2027.

This creates a liquidity event. The investor must have cash available to pay the deferred tax—at the federal level, 23.8% of $3 million is $714,000—even though the QOF investment remains illiquid and cannot be sold without forfeiting the ten-year exclusion. Sophisticated investors are planning for this in one of three ways. First, reserve cash: set aside the estimated tax liability in a money-market account earning 5%, so the funds are available in April 2027. Second, refinance the QOF asset: if the property has appreciated and stabilized, pull cash out via a refinance in late 2026 to cover the tax bill. Third, sell a different asset: liquidate a non-QOZ investment in 2026 to generate the cash, effectively using the QOZ deferral to time the recognition of two gains.

The deadline also imposes a strategic constraint on new QOZ investments. An investor who recognizes a gain in 2025 and invests in a QOF by mid-2025 will pay tax on the deferred gain in April 2027—just 18–24 months after deployment. The deferral benefit is minimal, and the investor is effectively pre-paying for the ten-year exclusion. That is still economically rational if the property's expected appreciation is large, but it shifts the program's value proposition from deferral-plus-exclusion to exclusion-only.

QOZ vs. 1031 Exchange: Parallel Strategies for Different Constraints

Qualified Opportunity Zones and 1031 exchanges are both tax-deferral mechanisms, but they operate under different rules and serve different investor profiles. A 1031 exchange defers capital-gains tax by requiring the investor to acquire like-kind replacement property within 180 days; the deferral is permanent as long as the investor continues to exchange, but the gain is never excluded—it is merely rolled forward into the basis of each successive property. A QOZ investment defers the gain until December 31, 2026, and excludes 100% of the appreciation after ten years, but it requires that the replacement property be located in a designated census tract and satisfy the substantial-improvement test.

The choice depends on the investor's constraint set. An investor selling a $5 million Newport Beach duplex and seeking to acquire another coastal rental has two paths. The 1031 path: identify a like-kind property in Newport, Laguna, or Corona del Mar within 45 days, close within 180 days, defer the entire gain, and repeat the process at the next sale. The QOZ path: invest the gain amount into a QOF that acquires a property in a nearby QOZ tract (Santa Ana, Anaheim), execute a substantial-improvement program, hold for ten years, and exclude the appreciation. The 1031 path preserves location flexibility but offers no exclusion; the QOZ path sacrifices location flexibility but delivers a permanent exclusion.

Some investors layer the strategies. Example: an investor sells a $3 million property with a $1.5 million gain. She executes a 1031 exchange into a $2 million replacement property (deferring $1 million of the gain) and invests the remaining $500,000 gain into a QOF (deferring and ultimately excluding that portion). The result: she maintains a coastal rental in her preferred submarket via the 1031, and she captures the QOZ exclusion on a portion of the gain by accepting the census-tract constraint for that capital.

Submarket Selection: Gentrification Indicators and Ten-Year Appreciation Thesis

The QOZ program's ten-year hold requirement demands that investors underwrite not just current fundamentals but the trajectory of neighborhood change. A census tract that qualifies as low-income today may be a high-rent, supply-constrained submarket in 2035—or it may remain economically stagnant. The difference is the appreciation thesis, and it depends on observable gentrification indicators.

We track six leading indicators across coastal California QOZ tracts. First, retail lease velocity: the number of new restaurant, coffee, and boutique retail leases signed in the past 24 months. A tract that has added three or more chef-driven restaurants or specialty retail concepts is signaling demand from higher-income residents. Second, building permit activity: the volume of permits for residential additions, ADUs, and single-family renovations. Homeowners invest in improvements when they expect the neighborhood to appreciate. Third, school enrollment trends: rising enrollment at the neighborhood elementary school indicates that families are moving in, a proxy for perceived safety and quality of life. Fourth, crime rate trajectory: a 20%+ decline in property crime over three years is a strong signal that the submarket is stabilizing. Fifth, transit investment: proximity to a planned or under-construction light-rail station, bus rapid transit line, or bike infrastructure. Sixth, employment cluster proximity: distance to a major job center (university, hospital, corporate campus, life-sciences park) that is expanding headcount.

A QOZ tract that scores positively on four or more of these indicators is a high-conviction candidate for a ten-year hold. A tract that scores positively on fewer than two is speculative, and the investor should model a wider range of exit cap rates and rent-growth scenarios.

Exit Strategy: Selling the QOF Interest and Electing the Step-Up

The QOZ program's permanent exclusion is realized when the investor sells the Qualified Opportunity Fund interest after ten years and elects to step up the basis to fair market value. The mechanics are straightforward but require careful documentation. On the date of sale, the investor files an election with the IRS (on Form 8997) to adjust the basis of the QOF interest to its FMV, excluding the appreciation from taxable income. The election is irrevocable and must be made on a timely-filed return for the year of sale.

The exit itself can take several forms. The most common: the QOF sells the underlying property to a third-party buyer, distributes the proceeds to the investor, and the investor reports the sale of the QOF interest. The investor's basis in the QOF interest is stepped up to the FMV of the distributed proceeds, so the gain is zero. Alternatively, the investor can sell the QOF interest itself to another investor, though the market for QOF interests is thin and buyers typically demand a discount to NAV.

Timing the exit is critical. The ten-year hold period is measured from the date the investor acquired the QOF interest, not the date the QOF acquired the property. An investor who contributed capital to a QOF on March 15, 2025, must hold the interest until March 15, 2035, to qualify for the exclusion. Selling even one day early disqualifies the investment, and the appreciation is fully taxable. Investors should calendar the ten-year anniversary and begin marketing the property 12–18 months in advance to ensure a sale closes after the deadline.

Risk Factors: Regulatory Change, Market Cycles, and Execution

The QOZ program is federal law, but it is not immune to legislative risk. Congress has debated modifications to the program since its inception—proposals to tighten the substantial-improvement test, limit the exclusion to primary residences, or sunset the benefit entirely. While no changes have been enacted, investors should model the possibility that future legislation could cap the exclusion amount or impose additional compliance requirements. The ten-year hold period spans multiple election cycles, and tax policy is subject to change.

Market risk is inherent in any long-duration real estate investment. A property acquired in 2025 will be sold in 2035, and the exit environment—interest rates, cap rates, rent growth, buyer demand—is unknowable today. Coastal California has historically been resilient, but the region is not immune to economic cycles. The 2008–2012 downturn saw coastal rents decline 15–20% peak-to-trough, and cap rates expanded 200+ basis points. An investor who underwrites a 4.7% exit cap and realizes a 6.2% exit cap will see the property's value decline by 24%, erasing much of the appreciation and reducing the exclusion's value.

Execution risk—construction delays, cost overruns, lease-up shortfalls—is the most controllable but also the most common failure mode. The substantial-improvement test is unforgiving, and a project that misses the 30-month deadline loses QOZ status. Investors should work with experienced general contractors, budget 20% contingency on hard costs, and secure entitlements before closing the acquisition.

Case Study: Santa Ana Arts District Four-Unit New Construction

We modeled a representative QOZ investment to illustrate the program's economics. The asset: a 5,000-square-foot vacant lot in Santa Ana's QOZ tract 06059074604, zoned for four residential units by right, located three blocks from the Downtown Santa Ana OCTA station. The investor acquired the lot in February 2025 for $650,000, contributed $2.1 million of deferred capital gains to a QOF, and the QOF is constructing a four-unit building with an all-in basis of $2.75 million (land plus hard costs, soft costs, and financing). The project will deliver in November 2026, satisfying the substantial-improvement test with 21 months to spare.

Pro forma: each unit is 1,100 square feet, two bedrooms, two baths, with in-unit laundry and one parking space. Asking rent is $3,400/month, a 6% premium to the submarket median for new construction. Stabilized NOI is $142,000 (after 5% vacancy, 25% operating expenses, and $18,000 annual reserves). Year-one cap rate: 5.2%. The investor models 6.8% annual rent growth (in line with the tract's trailing five-year average), 50-basis-point cap-rate compression by year ten (as the neighborhood gentrifies and institutional buyers enter), and a 4.7% exit cap.

Ten-year projection: year-ten NOI is $270,000, exit value is $5.74 million, gross gain is $2.99 million. Under the QOZ structure, the $2.99 million appreciation is excluded, saving $711,000 in federal tax. The investor also pays tax on the $2.1 million deferred gain in April 2027 (less the 10% step-up, so $1.89 million taxable), for a tax bill of $450,000. Net tax savings: $261,000, or 9.5% of the all-in basis. After-tax IRR: 13.7%, versus 11.4% for an identical non-QOZ investment. The 230-basis-point spread is the program's value creation, and it compounds over the ten-year hold.

Action Plan: Deploying Capital Before the Window Closes

The QOZ opportunity is time-sensitive. Investors who have realized or expect to realize capital gains in 2025 should begin the site-selection and underwriting process immediately. The 180-day reinvestment window is firm, and the substantial-improvement test requires that the investor have a clear construction plan and financing in place before closing the acquisition.

Step one: identify the gain event. Stock sale, business sale, real estate sale, partnership distribution—any realization event starts the 180-day clock. Step two: map the QOZ tracts in your target geography. The Treasury's online tool (https://www.cdfifund.gov/opportunity-zones) provides shapefiles and census-tract boundaries; overlay those with your submarket knowledge to identify high-conviction candidates. Step three: underwrite the substantial-improvement budget. Work with an architect or contractor to estimate hard costs and confirm that the improvement budget will exceed the purchase price. Step four: structure the QOF. Most investors use a single-asset QOF (one fund, one property) to simplify compliance and avoid cross-collateralization. Step five: secure financing. Approach lenders with QOZ experience and lock a rate before closing. Step six: close and deploy. Contribute the gain amount to the QOF within 180 days, acquire the property, and begin construction.

The investors who execute this sequence in 2025 will hold a tax-free call option on a decade of coastal California appreciation. The investors who wait will pay full freight.

Frequently Asked Questions

What is the deadline to invest in a Qualified Opportunity Zone to receive any tax benefit?

Can I use a QOZ investment to defer capital gains from stock sales or business sales, or only real estate?

What is the substantial-improvement test, and how do I satisfy it?

How does the QOZ permanent exclusion compare to a 1031 exchange?

What happens to my deferred gain on December 31, 2026?