What Proposition 19 Changed—and What It Didn't

Proposition 19 passed in November 2020 and took effect February 16, 2021. It replaced two long-standing parent-child and grandparent-grandchild exclusions under Proposition 58 (1986) and Proposition 193 (1996) with a single, narrower rule. Under the old regime, parents could transfer up to $1 million of assessed value for any property, plus an unlimited amount for a primary residence, without triggering reassessment. Children inherited the parent's Prop 13 base year, often dating to the 1970s or 1980s, and continued paying taxes on that artificially low assessed value even as market values climbed into the millions.

Prop 19 ended that arrangement for non-primary properties. The new law allows a parent-child exclusion only when the child uses the transferred property as their principal residence within one year of the transfer and continues to occupy it. Even then, the exclusion is capped: the child inherits the parent's base-year value plus $1 million. Any market value above that sum is reassessed at current rates. For rental properties, vacation homes, and investment real estate, there is no exclusion at all—transfer triggers immediate reassessment to fair market value, and the annual property tax resets accordingly.

The law did preserve one benefit: it expanded the portability of Prop 13 basis for seniors, disabled persons, and wildfire/disaster victims who sell a primary residence and buy another anywhere in California. That portability piece—allowing homeowners age 55+ to transfer their low tax base up to three times in a lifetime—was the voter-facing sweetener that helped Prop 19 pass. But for landlords and real estate investors, the headline is the loss of the rental-property exclusion.

Reassessment Mechanics and Timing

When a non-exempt transfer occurs, the county assessor recalculates the property's assessed value using the lesser of the current market value or the purchase price (if an arm's-length sale). For inherited property, market value is determined as of the date of death or the date the deed is recorded, whichever is later. The new assessed value becomes the base year for future Prop 13 calculations, which then grow at a maximum of 2% per year until the next change in ownership.

The reassessment is not retroactive, but it is immediate. If a parent dies in March and the property transfers in April, the new tax bill reflects the higher assessed value starting with the next fiscal year (July 1 in California). Supplemental assessments may issue mid-year to true up the difference. For a coastal rental that has appreciated significantly since the original purchase, the tax increase can exceed the property's annual net operating income, rendering the asset uneconomic to hold.

The Coastal California Impact: A Tale of Two Eras

Coastal California—from San Diego County through Orange County, Los Angeles, Ventura, Santa Barbara, and up the Central Coast—has seen some of the state's most dramatic long-term appreciation. A single-family rental purchased in Huntington Beach in 1978 for $110,000 might carry a Prop 13 assessed value of $160,000 today (after forty-five years of 2% annual increases), generating an annual tax bill around $1,760. That same home now appraises at approximately $2 million or more. Under Prop 19, an heir who does not occupy the property will see the assessed value jump to current market value, and the tax bill to roughly $20,000 or more per year—a substantial increase.

The math is even more severe in markets like Newport Beach, Manhattan Beach, La Jolla, and Palos Verdes, where legacy properties acquired in the 1970s and 1980s now command $3–$8 million. In those cases, the annual tax reset can exceed $50,000–$80,000, wiping out cash flow and forcing a sale within months of inheritance.

For a Newport Beach duplex acquired in 1985 at $240,000 and now worth approximately $3 million or more, reassessment can significantly increase the annual tax bill, potentially turning a cash-flowing asset into a forced sale.

Case Study: Orange County Duplex

Consider a two-unit property in Costa Mesa purchased in 1987 for $285,000. The current Prop 13 assessed value, after thirty-six years of 2% growth, sits at approximately $580,000, yielding an annual property tax of approximately $6,380. Each unit rents for approximately $3,400 per month, generating approximately $81,600 in gross annual income. After insurance ($2,800), maintenance ($4,500), management fees at 5.9% ($4,814), and property tax, the net operating income is roughly $63,100, or approximately a 10.9% cash-on-original-cost return.

The property's current market value is approximately $1.95 million. If the owner passes away and the heir does not move into one of the units, Prop 19 triggers reassessment to current market value. The new annual tax bill jumps to approximately $21,450—an increase of approximately $15,070. Net operating income falls to approximately $48,030, and the cash-on-market-value yield drops to approximately 2.5%. At that margin, the property may no longer pencil as a hold, and the heir may consider listing within a reasonable timeframe.

The Primary-Residence Exception: Rules and Limits

Prop 19 does preserve a partial exclusion when the transferred property becomes the child's primary residence. To qualify, the child must:

- File a claim with the county assessor within one year of the transfer (death or deed recordation).

- Occupy the property as their principal residence within one year and maintain that occupancy.

- Demonstrate that the home is their primary residence for tax purposes (voter registration, driver's license, tax return filing address).

When these conditions are met, the child inherits the parent's Prop 13 base-year value plus an additional $1 million in assessed value. Any market value above that combined figure is reassessed. For example, if the parent's assessed value was $400,000 and the home's current market value is $2.3 million, the child's new assessed value becomes $1.4 million (the $400,000 base plus $1 million). The difference—$900,000—is reassessed, adding roughly $9,900 to the annual tax bill.

This exception is meaningful for heirs who genuinely intend to live in the inherited home, but it offers no relief for rental properties, vacation homes, or investment real estate. And even for primary residences, the $1 million cap means that high-value coastal properties still face significant reassessment. A home valued at $5 million in La Jolla with a $300,000 Prop 13 basis will reset to $1.3 million under the exclusion, leaving approximately $3.7 million subject to reassessment and an annual tax increase of roughly $40,700.

Strategic Responses for Coastal Landlords

The loss of the parent-child exclusion for rental property has forced a wholesale rethink of succession planning. The strategies below represent approaches that coastal California investors, estate planners, and tax advisors commonly explore.

Pre-Transfer Sale and Reinvestment

One option is for the parent to sell the property before death and reinvest the proceeds in a way that benefits the heirs without triggering Prop 19. A 1031 exchange into a newer, lower-basis property in a higher-growth market can reset the clock, giving the family a fresh Prop 13 base year and reducing the reassessment shock when the next transfer occurs. Alternatively, the parent can sell, pay capital gains tax (often at favorable long-term rates, with a partial exclusion if the property was once a primary residence), and gift the after-tax proceeds to the children, who then purchase their own investment properties with a current-market basis.

This approach sacrifices the step-up in basis that heirs would receive at death (under IRC Section 1014, inherited property gets a basis equal to fair market value at death, erasing all pre-death capital gains). But it avoids the Prop 19 reassessment trap and gives the family liquidity and flexibility. For properties with modest embedded gains or where the parent has significant capital-loss carryforwards, a pre-transfer sale can be tax-efficient.

Strategic Occupancy by the Heir

If the heir is willing and able to occupy the property as their primary residence, the Prop 19 exclusion can preserve a meaningful portion of the Prop 13 basis. This strategy works best when:

- The property is a single-family home or condo suitable for year-round occupancy.

- The heir does not already own a primary residence (or is willing to sell it).

- The market value is close enough to the parent's basis that the $1 million cap covers most of the appreciation.

- The heir plans to hold the property long-term, allowing the Prop 13 basis to grow at 2% per year and the market value to appreciate further.

In practice, this means the heir moves into the inherited home within twelve months, files the claim, and remains there for at least a few years to satisfy the assessor's scrutiny. After that period, the heir can convert the property back to a rental (triggering no additional reassessment, since change-in-use is not a change-in-ownership under Prop 13) and enjoy the preserved low tax basis for as long as they own the asset.

Entity Structuring and Lifetime Gifting

Some families have explored holding rental property in LLCs, family limited partnerships, or irrevocable trusts, hoping to avoid the Prop 19 reassessment by transferring entity interests rather than the underlying real estate. California law, however, treats a change in ownership of the entity as a change in ownership of the property when more than 50% of the ownership interests transfer within a rolling three-year period. This means that simply gifting LLC membership units to children over time will eventually trigger reassessment once the cumulative transfers exceed the 50% threshold.

That said, entity structures can still offer value for estate-tax planning, liability protection, and facilitating partial gifts during the parent's lifetime. By gifting small percentages of the LLC each year (staying below the 50% cumulative trigger), parents can begin transferring wealth while retaining control and deferring the reassessment event. When the parent dies, the remaining interests transfer, the 50% threshold is crossed, and reassessment occurs—but by then the children may have received years of income distributions and built up liquidity to handle the higher tax bill or execute a sale.

Installment Sale to Heirs

An installment sale allows the parent to sell the property to the child over time, with the child making annual payments (often secured by a promissory note). The parent recognizes capital gain ratably as payments are received, spreading the tax liability across multiple years. The child takes a basis equal to the purchase price, which is typically set at fair market value, so there is no Prop 13 benefit—but there is also no Prop 19 reassessment surprise, because the transaction is a voluntary sale, not an inheritance.

This strategy works when the child has income or financing capacity to make the installment payments, and when the parent wants to convert the property into a stream of retirement income rather than holding it until death. The installment note can be forgiven in the parent's will, but that forgiveness is treated as a bequest and may trigger reassessment under Prop 19 if the property is not the child's primary residence. Careful drafting is essential.

Modeling the Decision: Hold, Transfer, or Sell?

Every family's situation is different, but the decision tree generally follows this logic:

- Calculate the reassessment impact. Determine the current Prop 13 assessed value, the current market value, and the difference. Multiply the difference by approximately 1.1% (a commonly cited effective property tax rate in many coastal counties) to estimate the annual tax increase.

- Model post-reassessment cash flow. Subtract the new tax bill from the property's current NOI. If the result is negative or below a 3–4% cash-on-value return, the property may be unsustainable as a hold.

- Assess the heir's occupancy intent. If the heir will occupy the property as a primary residence, calculate the benefit of the $1 million exclusion and compare the resulting tax bill to the cost of the heir's current housing. Often, moving into the inherited home—even with a higher tax bill—is cheaper than renting or buying elsewhere in the same market.

- Evaluate sale alternatives. Model a sale at current market value, net of transaction costs (typically 6% commission, 1% closing costs, and capital gains tax at the parent's or heir's marginal rate). Compare the after-tax proceeds to the present value of holding the property with the higher tax bill.

- Consider 1031 repositioning. If the family wants to remain in real estate, a 1031 exchange into a newer property with a higher basis and stronger cash flow can reset the economics and defer the capital gain.

In most cases, the math points toward one of three outcomes: the heir occupies the home and preserves the basis; the family sells and redeploys the capital; or the family holds for a few years, harvests the remaining cash flow, and then sells when the tax burden becomes untenable. The investors who modeled these scenarios in 2021 and 2022 were better positioned to make informed decisions and avoid forced sales.

Compliance and Filing Requirements

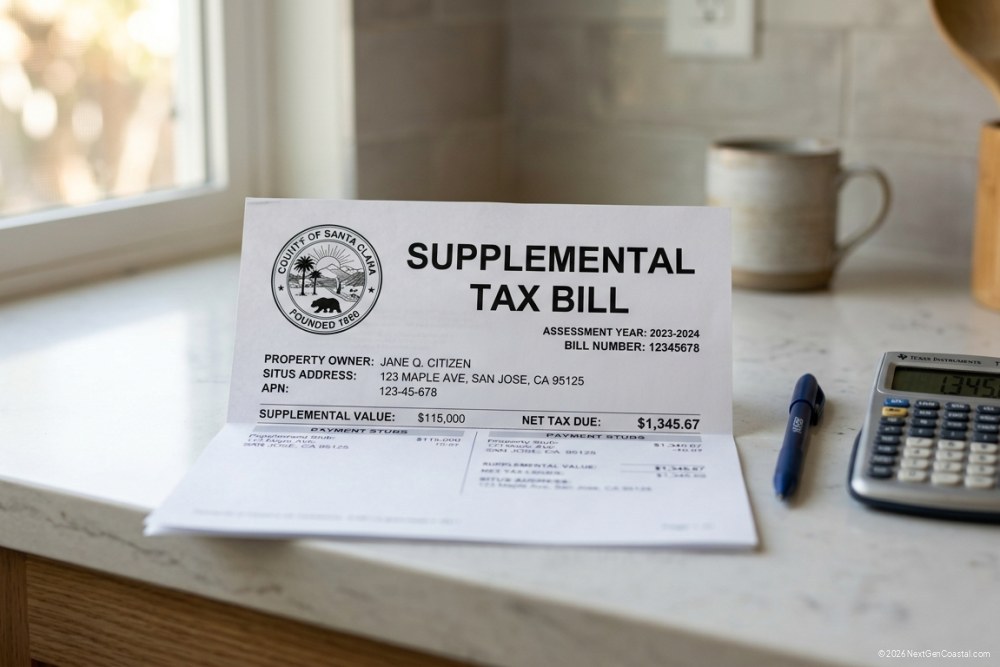

Heirs who qualify for the primary-residence exclusion must file a claim with the county assessor within one year of the date of transfer. The claim form—typically the BOE-19-P in most counties—requires documentation proving occupancy: a copy of the death certificate, the recorded deed, a driver's license showing the property address, voter registration, and utility bills. Failure to file within the one-year window forfeits the exclusion, and the property is reassessed at full market value with no appeal.

For properties that do not qualify for the exclusion, no filing is required—the assessor will automatically reassess based on the recorded deed and the property's market value. Heirs should expect a supplemental tax bill within a few months of the transfer, covering the difference between the old and new assessed values for the remainder of the fiscal year.

Market Effects: Forced Sales and Inventory

Prop 19 has had a measurable impact on coastal California's housing inventory. In the years following its implementation, estate sales and family-transfer listings increased in high-appreciation markets like Orange County and coastal Los Angeles. Many of these properties had been held by the same family for decades and were never intended for sale, but the reassessment math left heirs with difficult decisions.

This inventory activity has created opportunities for buyers, particularly in the $1.5–$3 million segment where legacy single-family rentals and small multifamily properties cluster. Heirs often price competitively to manage carrying costs, and many properties come to market in as-is condition, creating opportunities for value-add investors. At the same time, the loss of these long-held, low-basis assets has reduced the supply of cash-flowing rentals in the hands of multi-generational landlords, shifting ownership toward institutional buyers and newer investors with higher cost bases and shorter hold periods.

Looking Ahead: Legislative and Legal Challenges

Prop 19 has faced legal challenges on equal-protection and due-process grounds, with opponents arguing that the law unfairly discriminates between heirs who can afford to occupy an inherited property and those who cannot. As of early 2025, these challenges have not resulted in changes to the law, and Prop 19 remains in effect. There is no significant legislative momentum to repeal or amend Prop 19, in part because the revenue it generates has become embedded in county budgets.

For landlords and investors, the takeaway is clear: Prop 19 is the current law, and the old strategies no longer work. Families with coastal rental property must plan proactively, model the reassessment impact, and make decisions—occupancy, sale, or restructuring—well before the transfer occurs. The families who wait until after the parent's death to think about Prop 19 are the ones who face the most limited options.

NextGen Coastal's Approach to Prop 19 Transitions

At NextGen Coastal, we work with heirs and estate executors navigating Prop 19 transitions across Orange County, Los Angeles, and San Diego. Our process begins with a cash-flow model: we pull the current Prop 13 assessed value from county records, order a broker price opinion or desktop appraisal to establish market value, and calculate the post-reassessment NOI. If the property pencils as a hold, we help the heir file the primary-residence claim (when applicable) and transition the asset into our management platform. If the math points toward a sale, we coordinate with the family's estate attorney and CPA to time the transaction, model 1031 exchange scenarios, and connect the executor with vetted listing agents who understand the dynamics of estate sales.

For properties that fall into the gray zone—marginal cash flow, uncertain heir intent—we often recommend a short-term hold strategy: keep the property rented for 12–24 months, capture the remaining cash flow, and revisit the decision once the heir's housing situation and financial picture clarify. Our proprietary platform tracks the reassessment timeline, flags filing deadlines, and generates monthly reports showing actual vs. projected NOI, so families can make informed decisions with full visibility into the numbers.

We also see Prop 19 creating opportunities for our investor clients. Estate sales often come to market at competitive prices, and sellers are motivated to close efficiently. For buyers with capital and a long-term hold horizon, these properties offer a chance to acquire coastal real estate, reset the basis to current market value, and build a new Prop 13 base year that will compound at 2% annually for decades. Investors who acted in recent years—buying estate-sale inventory at competitive prices—have positioned themselves to benefit from rent growth and appreciation.

Conclusion: The New Playbook for Intergenerational Wealth

Proposition 19 fundamentally changed the economics of passing rental property to the next generation in California. The unlimited parent-child exclusion that allowed families to hold coastal real estate across multiple generations—preserving older tax bases into the 2020s—is gone. In its place is a narrow, conditional exclusion that requires occupancy and caps the benefit at $1 million, leaving high-value properties exposed to reassessment that can significantly increase the annual tax bill.

For coastal landlords, the path forward requires early planning, rigorous financial modeling, and a willingness to make informed choices. Some families will choose occupancy, moving the next generation into the inherited home and preserving the Prop 13 basis for another cycle. Others will sell, take the capital gain, and redeploy into assets with better cash flow or lower tax exposure. Still others will hold for a few years, harvest the remaining income, and then sell when the reassessment burden becomes unsustainable.

What no longer works is the old default—inherit, hold, and pass down again—because the tax math no longer supports it. Prop 19 forces a reckoning, and the families who face that reckoning proactively, with clear-eyed analysis and professional guidance, are the ones who preserve wealth and maintain control over their options. The window to act is narrow: once the transfer occurs, the reassessment is automatic, and the options narrow quickly. The time to plan is now, while the parent is still living and the family can model scenarios, explore alternatives, and make decisions on their own timeline rather than the county assessor's.

Frequently Asked Questions

Does Prop 19 apply to rental properties inherited before February 16, 2021?

Can I avoid Prop 19 reassessment by holding the property in an LLC?

What happens if I inherit a rental property and decide to move into it a year later?

How does Prop 19 interact with the step-up in basis for capital gains tax?

Can I rent out part of an inherited home and still claim the Prop 19 exclusion?